ACGL, whose promoters are Tata Motors and the Govt of Goa, is one of India's largest bus-body manufacturers. It also produces sheet metal components. But things just haven't gone ACGL's way. I honestly feel bad for the company's management.

- In 2007, the company raised money through a rights issue to double capacity. And then the global economic crisis hit. Talk about perfect timing! Bus exports fell and ACGL, with its expanded capacity and lesser demand, suffered a lot.

- The company had decided to move its sheet metal business to Pune, to make Goa a dedicated bus-body manufacturing operation, since the scale had increased. Of course, then the global economic crisis hit and this plan had to be shelved. The company has now bought a plot at Dharwad for this purpose.

- Well, things improved gradually and the company seemed to be limping back to normal. But then, Murphy's Law!! The labour union declared a strike and also prevented any workers from entering the premises. The seriousness of the strike can be judged from this article.

Well, feeling bad for the management and all is fine, but the critical question is, does the company have any value? Now since the company is going through a really bad phase, lets try and find out the bare minimum valuation that can be given to the company;

ACGL is being valued by the market as given. It is important to remember that the cash on books is because of the company's rights issue and is not fully internally generated.

Anyway, the company has two divisions, Sheet Metal Components and Bus Body Building.

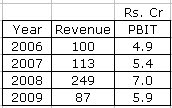

The Sheet Metal Component Division is smaller in size and is profitable. This division's performance was hit in 2009 because of closure, for shifting to another location.

So what kind of valuation should one give to this division? Since we are trying to calculate the minimum value of the business, let us value it at 4x FY08 PBIT of Rs.7 crores. This division may be valued at Rs.28 crores.

Moving on, to the bigger and more important Bus Body Division;

- This division has not performed efficiently. In 2009, the PBIT per bus body was down to a record level of Rs.35307/-. This was essentially because the company got more orders for smaller buses, in which margins are lesser.

- The current capacity of the division is 4800 bus bodies. The only thing lacking is orders!!! As and when the operations become normalised, the company should be able to sell at least 4500 bus bodies a year, generating PBIT of at least Rs.18 crores at Rs.40000 PBIT/bus body. Both these numbers have been deliberately taken on the lower side. (In fact, all requirements for hiking this capacity to 10000 bus bodies are complete).

Ok, let's day-dream here a bit. Let's suppose that the scenario improves drastically and the company manages to get large orders on the domestic as well as foreign front. It is able to operate at full capacity of 10000 buses! What would happen then? Even if we consider PBIT/bus body of Rs.40000/-, the potential for PBIT of at least Rs.40 crores exists!

Those numbers felt nice huh? Good, now back to reality! :-)

One can surely give this business a value of 8x PBIT, resulting into a 'normalised' valuation of Rs.144 crores. (Rs.18 crores x 8 times)

So let us see what can the fair value of the business be;

I have assumed that cash Rs.25 crores has been eroded during FY10. Hence, in the adjoining valuation, cash has been taken as only Rs.40 cr. The valuation works out to Rs.212 cr against present market cap of Rs.147 cr!! Sweeeeeeet!!!

Well, before you place the 'buy' order with your broker, please read The Good, The Bad and The Ugly of the company!!

The Good

- ACGL has strong promoters in the form of Tata Motors. TaMo has been supporting the company throughout its times of distress. TaMo has also increased its stake in ACGL over the last 2 years.

- The conservative valuation of ACGL works out to much more than the market cap.

- The business potential is huge. With rapid urbanisation and transportation requirements, large demand for buses is expected.

The Bad

- Due of one reason or the other, historically, ACGL has failed to deliver and live up to its potential.

- Our valuation is at 'normalised' operations. When will the operations normalise? Well, thats anybody's guess. Absolutely no visibility is there.

The Ugly

- ACGL's promoters (Tata Motors) have a JV in India with one of the world's largest bus body manufacturers, Marcopolo. Details can be read here. In my view, this is a huge conflict of interest. The promoter has a JV, which competes directly with its subsidiary! So how does TaMo divide its business between its JV and its subsidiary? Not really clear. Big risk here..

Well, to conclude, one can say that ACGL definitely has value. The key question is, when will the company get back on track so that this value gets unraveled? Or will Murphy's Law continue to wreck havoc with ACGL? Time will tell...

Cheers!

5 comments:

you have nice blog

We Manufacturers and Suppliers of Clutch Plates (Rubber based , Cork based & Paper based) for Two & Three wheelers, Disc Brake Pads for Two, Three & Four wheelers, Fine Blank, Sheet Metal Components, Pressure Die Caste & Forged ( Machined) Components for automotive industries.

o ok..umm,well, gud for you i guess! :-|

Neeraj

Neeraj,

whats your take on the current valuations of ACGL?

Neeraj,

whats your take on current valuation of ACGL and if one can enter at cmp if ots looks good for a year of two?

Hello Anon,

Competition has increased quite a lot..the business is still not doing well. Value is surely there, but when will that be discovered remains unknown. I feel that better opportunities might be available than acgl.

cheers!

Neeraj

Post a Comment