Now that we have the 'happy new year' and all out of the way, lemme come to the point. Alembic Ltd is executing a demerger scheme. Let us see if there is any money to be made here.

The scheme:

- Under the scheme of demerger, the first part of the business (the good part) will be transferred to Alembic Pharma Ltd. (Alembic Pharma (APL) is currently a wholly owned subsidiary of Alembic Ltd.)

- Alembic will retain the second part (PenG business, land, power assets).

- The total debt of Alembic will be split into 85%(APL) and 15%(Alembic)

- Shareholders of Alembic holding 1 share will get 1 share in Alembic Pharma.

The shareholding:

Public holding in APL would be lesser, since Alembic already holds some shares in APL.

The facts:

- Currently, the market is valuing Alembic at Rs.900 cr mkt cap and EV of about Rs.1280 cr. On a PE basis, the stock is currently quoting at about 20x.

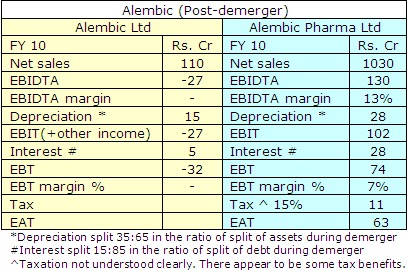

- The pre-demerger numbers of Alembic also include those of PenG division. This is a loss making division of the company, with Rs.115 cr revenues and Rs.24 cr loss before tax for FY10.

- If the FY10 numbers are split to reflect the demerger effect, it would be as follows:

The opportunity:

Let us try and value the two businesses separately:

Alembic Pharma Ltd:

- This company would contain the API and formulations business (domestic as well as export). FY10 revenue attributable for this company was Rs.1030 cr, with operating profit margins of around 12.7% and PBT margin of 6.8%. EBITDA of Rs.130 cr and EBT of Rs.74 cr.

- The business is profitable and growing at 10-12%. APL also has recognized brands such as Althrocin, Roxid and Azithral in its portfolio.

- Post demerger, APL would have no further need of expansion. Consequently, the free cash generated by the business would be utilized for repayment of debt. (APL debt Rs.350 cr. Alembic total cash from operations for FY10 Rs.127 cr). Consequently, in the EV, the debt should be replaced by market-cap going forward next couple of years.

- Alembic’s peers and companies in the sector quote at premium valuations, as much as 12x EV/EBITDA and 24x TTM EPS.

- Valuing Alembic at lower multiples of 10x EV/EBITDA(FY10) and 15x FY10 PAT, market cap comes to around Rs.950 cr. Value per share = 950/18.84 = Rs.50/- (to be used as a reference only).

Alembic Ltd:

- Post demerger, Alembic will be left with the loss making PenG business, land and power assets. Also, it will have 29.5% stake in APL. Residual assets of Alembic would be Rs.250 crores, which is 35% of gross block.

- On a conservative basis, I would value the PenG business at ZERO (although it certainly should be accorded some value).

- Alembic will hold 29.5% of APL, which is worth Rs.280 cr. I am giving a 90% haircut to this and taking only 10% of the value, Rs.30 cr. (Pessimistic calculations help provide some MOS)

- The power assets consist of 3 cogen plants, total 11 MW and 4 windmills of total 5 MW. Since they are used for captive consumption, I would accord them ZERO value.

- Alembic would also have land of 115 acres at Vadodara. Out of this, the manufacturing facilities occupy about 45 acres. So what should be valued is only 70 acres. As per information obtained, the land rate in the area is Rs.600-700 per sq.ft. I would value the land at Rs.500/sq.ft. Valuation works out to Rs.140 cr.So, the residual business of Alembic may be valued at Rs.30 cr + Rs.140 cr = Rs.170 cr, or Rs.13 per share.

Total valuation comes to Rs.63 per share. (Rs.50 for APL and Rs.13 for Alembic)

To sum up:

- Dilution in APL is killing off possible arbitrage in the deal.

- To get some margin of safety, stock can be bought below Rs.55 per share.

- There is a probability that BOTH the companies may get delisted for some period of time. (Got to get clarification from the CS on this).

- regarding the time involved in this deal happening, the management had this to say in a recent TV interview: "The demerger is in process right now. We are awaiting some final approvals which we should hopefully get by the end of December and if all the timelines go well then hopefully by about March we will look at listing a separate company."

At CMP of 67 bucks, I do not think there is much money to be made. Lets hope that the stock drifts down. Position should be taken only if the stock comes at a price where there is comfort.

Cheers and happy investing!